CPI climbed to 2.8%

BoC Policy Rate 5.0%

CPI Trim 3.1%

Bank Prime Rate 7.20%

March 19, 2024

Bank of Canada's Next Rate Announcement June 5th, 2024

Canada's economic landscape is once again being influenced by inflation, which has taken center stage. Recent data from Statistics Canada has revealed an unexpected slowdown in the country's annual inflation rate, dropping to 2.8 percent in February 2024. This deceleration holds significant implications, especially for homeowners and potential mortgage seekers, as it intersects with the trajectory of interest rates.

With approximately 60% of Canadian mortgages set for renewal in the upcoming years, understanding the impact of inflation and potential interest rate adjustments is crucial. For these homeowners, any decrease in interest rates could lead to substantial reductions in their overall interest expenses, providing much-needed financial relief in an uncertain economic environment. The possibility of lower interest rates, driven by moderating inflation, brings hope to individuals navigating the renewal process.

Moreover, the immediate impact of today's announcement on bond yields cannot be overlooked. The downward shift in bond yields, prompted by expectations of rate cuts, directly affects fixed mortgage rates. As bond yields decline, lenders may adjust their fixed mortgage rates accordingly, allowing homeowners and prospective buyers to secure favorable rates. This dynamic highlights the intricate relationship between inflation, central bank policies, and mortgage rates, underscoring the importance of staying informed and proactive in financial decision-making.

For homeowners, particularly those with variable-rate mortgages or individuals contemplating entering the housing market, understanding the dynamics of inflation and its effects on interest rates is essential. Inflation acts as a gauge for central banks in shaping monetary policy, particularly interest rates. As inflation eases, central banks may opt to lower interest rates to stimulate economic growth and stabilize prices. Conversely, central banks may raise interest rates when inflation surges to control excessive spending and maintain price stability.

The anticipated cycle of rate cuts could translate into favorable conditions for homeowners and mortgage seekers. Lower interest rates can lead to reduced mortgage payments, offering relief to existing homeowners and enhancing affordability for those looking to step into the housing market. Additionally, prospective buyers may find themselves in a more advantageous position to secure financing as borrowing costs decrease.

However, it is important to acknowledge that the impact of inflation and interest rates extends beyond mortgage rates. Inflation influences various aspects of household expenses, from groceries to telecommunications services. The recent data highlighted a slowdown in food price growth, although prices remained elevated compared to previous years. Furthermore, consumers observed significant declines in cellphone and internet service prices, contributing to the broader narrative of moderating inflationary pressures.

As consumers navigate these economic shifts, it is crucial to remain vigilant and adaptable. While the prospect of lower interest rates may offer immediate benefits to homeowners and mortgage seekers, it is essential to consider the broader economic implications. As interest rates fluctuate in response to inflationary trends, individuals should assess their financial strategies, including mortgage decisions, in light of evolving market conditions.

In conclusion, the unexpected deceleration in Canada's inflation rate has paved the way for potential changes in monetary policy, with implications for homeowners and mortgage seekers alike. Understanding the interplay between inflation, interest rates, and household finances is vital in navigating these economic shifts. As the economic landscape evolves, staying informed and proactive will be crucial in making well-informed financial decisions.

Stay tuned for updates as we continue to monitor the developments shaping Canada's economic landscape and their implications for homeownership and mortgage markets.

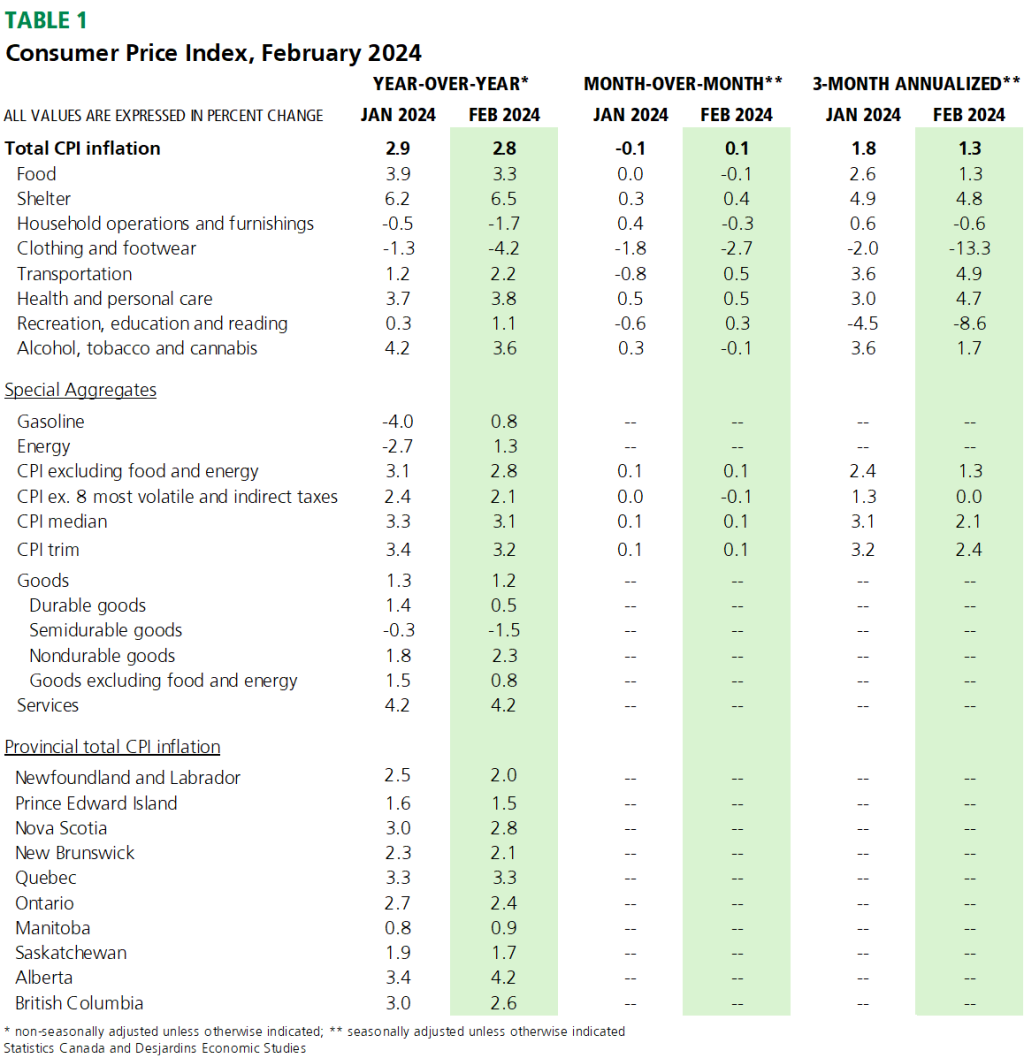

In February, the headline CPI climbed 2.8% compared to the same period last year, marking the second consecutive month where it fell below the consensus forecast of 3.1% by economists. Additionally, monthly prices inched up by 0.1% on a seasonally adjusted basis, reversing the decline seen in January. Key data points are outlined in Table 1 for reference.

Implications

Inflation in Canada remains a focal point in 2024, as February marked the second consecutive month of lower-than-expected figures. With inflation at 2.8% y/y, it appears to be settling comfortably within the Bank of Canada's target range of 1% to 3%.

Delving into the specifics of the February data, there were positive developments to note. The growth in food prices (2.4%) continued to slow down. Moreover, the impact of gasoline on inflation was modest despite a positive y/y reading. The overall CPI excluding food and energy closely tracked the 2.8% increase in headline inflation. Canadians also experienced declines in prices for cellular services (-26.4%) and childcare (-2.8%) during the month. However, there were some less favorable trends as well. Shelter prices saw an uptick on a y/y basis in February, driven by both rented (7.9%) and owned (6.9%) accommodations, with the latter primarily influenced by increasing mortgage interest costs (26.3%).

Inflation Announcement